“Straight Edge Finance” is a column written by Clark Troy, and presented by Red Reef Advisors

The wisdom of funding specific needs when markets are high

I just bought a new car a couple of weeks back, my first new car purchase ever.* It’s a beautiful new Toyota Prius plug-in hybrid, pretty much the car of my people, as a Chapel Hill native. We needed a fresh vehicle because the 2010 Prius we had bought in 2012 as a wee low-mileage thing and had christened “Beatrice” had come to that inflection point all cars reach where the cost of repairs exceeds its value. Our mechanic looked me squarely in the eye and delivered the sad verdict.

When discussing capital markets we often talk about not wanting to buy at the top or sell at the bottom, while noting that paradoxically one never knows when the actual tops and bottoms are, except retrospectively. Which is absolutely true. You don’t know when a market has reached its tippy top in a given market cycle.

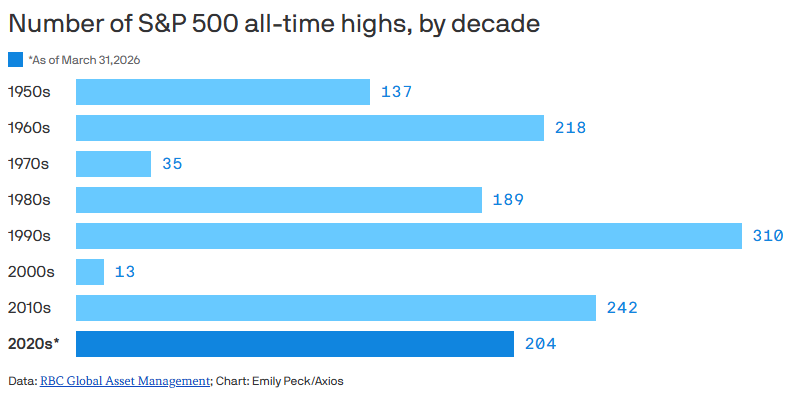

But while knowing “the peak” of a cycle is very hard, knowing when “a peak” has been reached is the easiest thing possible. And over the last decade the S&P 500 has hit new all-time highs some 204 times, which is a high number given that we’re only half way through the decade but not all that surprising given the propensity of both Democratic and Republican administrations to run huge deficits, thereby maintaining a large monetary supply, and also the general perception — which has gone away only in the last year and change — that the USA was the default best place for global investors to park wealth.

And when markets are at “a” peak, well that’s a great time to buy things that you need or just want. Like a car. Or a couch. Or a bathroom upgrade.

It’s a horrible feeling to look back when the markets have gone back down that you there was something worthwhile — be it a durable good or a long-deferred vacation — that you could have snatched up back when things were flush but you were too transfixed from warming yourself by the illusory glow of some numbers on a screen. That happens to people, particularly those who are relatively new to markets and caught up in the early-stage frisson of paper wealth. The behavioral economists most likely have a term for it but even if I went and refreshed my memory of what it was most of you would forget it posthaste because the term itself wouldn’t be relevant. We all regret missing opportunities to do something real for ourselves because we were counting our money, dreaming of what might be.

At the same time, we reasonably fear what is to come and our ability to maintain our current lifestyle as the future unrolls before us. How much money will we need to make it through to the end? How long will we live? How much money can we expect to earn on our investments through the decades? Good questions all, each of them precisely unanswerable in the present though all with guideposts if we’re willing to do research, observe ourselves honestly, and write things down. The only iron rule of finance is that those who earn and save more than they spend for most of their lives end up well off.

That sounds like a good place to end, but I can’t help but to loop back and look at the chart above with a couple of observations. First off, look how few all-time peaks the S&P 500 hit during the 2000s, and the 1970s for that matter. After the booyah 90s followed upon the post-Cold War End of History and the early, ecstatic days of the internet and the Nifty Fifty of demographically-driven expansion in the 1960s, markets had long rough periods. We know that history doesn’t repeat but it often rhymes. Could the 2030s also be a period of protracted challenges for the markets? They could. Nobody knows.

If that does happen, the 2030s should be a fine time to mend nets and for those earning salaries to contribute to 401ks, as were the aughts. For me, the decade to come should be a great time to own a relatively low-mileage Toyota and enjoy the PBJs that often comprise my breakfast, as will be the case today.

*I would never have contemplated buying new without the express counsel of my car-buying agent, who assured me that on this occasion the deal on the new car was better than any deals available on used cars for some nerdlinger technical reason long since jettisoned from memory.

Clark Troy was born in Durham and educated in the Chapel Hill-Carrboro City Schools, then elsewhere. He is a financial planner at Red Reef Advisors and may be reached at clark.troy@redreefadvisors.com. When not working, he reads, plays sports, blogs, naps, drinks coffee, studies languages and plays guitar, not necessarily in that order.

Clark Troy was born in Durham and educated in the Chapel Hill-Carrboro City Schools, then elsewhere. He is a financial planner at Red Reef Advisors and may be reached at clark.troy@redreefadvisors.com. When not working, he reads, plays sports, blogs, naps, drinks coffee, studies languages and plays guitar, not necessarily in that order.

For more from Clark, subscribe to his substack directly and check out other “Straight Edge Finance” columns in the full archive on Chapelboro

{kind=link}